Candy Crash

Sugar bashing and rise of raw materials price did not kill the German confectionery industry, but lack of innovation will

I am addicted to sugar.

A few months ago, I decided to go on a sugar detox to decrease my dependency on chocolates and pastries. The first weeks were extremely difficult, but it has been worth it. As I am a tracker freak, I started logging every time I ate sugar.

I went from consuming sugar nearly every day to doing so 40% of the time.

Ever since I have been obsessed with sugar.

I see Gummibärchen and lollipops everywhere. I notice how children get annoyed when parents refuse to buy a candy bag at the supermarket counter and how parents seem thrilled when they hide to eat a caramel-boosted chocolate bar.

Our cravings for sugary treats and insulin peaks contribute to the resilience of Haribo's homeland confectioners.

In this piece, I am covering:

How the German confectionery industry has been handling market pressures while maintaining its success.

However, the strategies employed although efficient do not seem robust

So what innovative directions this industry could consider?

The German confectionery industry has been sassily resilient

The German confectionery industry is comprised of companies manufacturers of cocoa, chocolate, and sugar confectionery selling their products via distributors who then resell them to the end consumers. These companies generated EUR 11bn of sales in 2022 and their revenues have been on an overall growth trend for the last 15 years with a minor decrease tendency from 2014 until COVID-19 hit.

The industry seems to have benefited from the pandemic, 2020 was the year with the second-highest growth rate (+8.2% vs. 2019) only behind 2022 which scored at +12% vs. 2021.

A confectionery manufacturer generated on average EUR 70 M of sales in 2022 and this has been steadily increasing during the last decade. This strength in sales reflects a healthy market for most of the companies, not just for the largest ones as there's general stability in the number of units.

Between 2019 and 2022, the industry lost “only” 5% of its capacity.

Confectionery companies aren't just surviving; they're making a greater impact by hiring more employees, whose productivity has soared over the past five years

This success is especially impressive in a difficult context

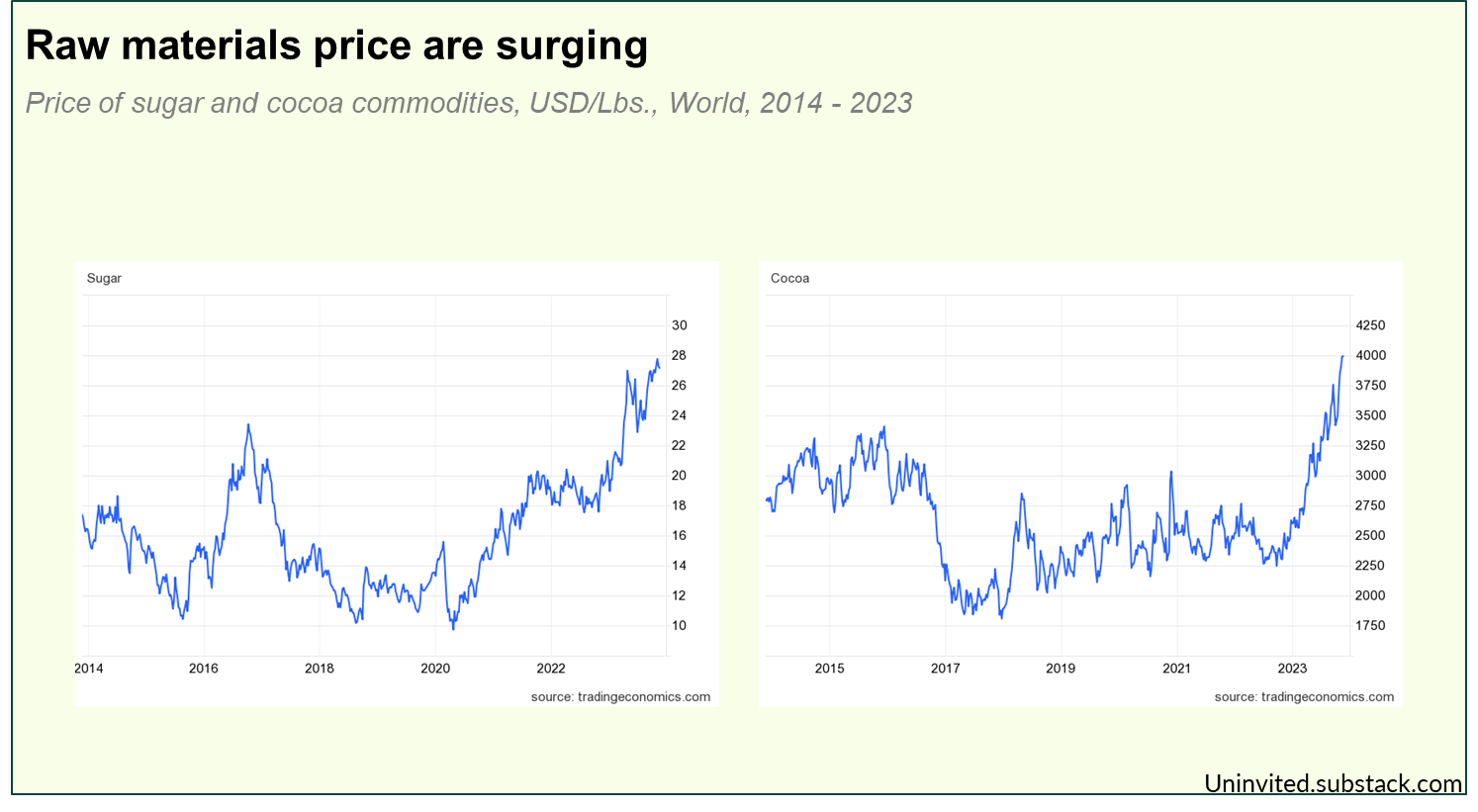

Raw materials like sugar and cocoa are the main input for the confectionery industry

Material costs make up 54% of the industry's expenses, mostly because of the need for raw materials like sugar and cocoa, and, unlike similar industries - such as baked goods and biscuits, confectionery relies more on these raw materials and less on human labor.

Commodities’ prices of the confectionery main input have exploded in the last few years

Sugar consumption has been openly criticized

There is more and more awareness of the health effects of sugar. Not a week passes without a documentary or article depicting the negative aspects of consuming sweet food and beverages.

The narrative often references scientific studies about sugar addiction and its health effects. Research papers on these subjects have nearly doubled in the past decade

Public policy initiatives, regulations,

and anti-sugar nudges are flourishing in Europe

While Germany has not implemented any direct measures yet, other countries in Europe have deployed sugar taxation and regulation in various forms.

France, Belgium, Finland, and Estonia have duty/taxes on soft drinks with added sugars, Norway taxes chocolate and sugar products at EUR 2.10/kg, and Hungary applies a public health tax with variable rates on sugar content for different food categories. EU regulations mandate nutrition declaration for amounts of sugars in prepacked foods and govern nutrition claims related to sugars, including 'sugars-free', 'no added sugars', and 'low sugars'

Although voluntary, the Nutri-Score labeling system is used by 860 brands in Germany and can discourage confectionery sales, directing consumers toward healthier choices.

The German confectionery is a EUR 11bn industry that has been growing at a 5% CAGR. The 154 companies have overall managed to succeed during and after the COVID-19 pandemic, in a context of raw materials surge and in an environment increasingly critical towards the negative effects of sugar and with more and more strict regulations.

How could the German confectioners thrive while facing such challenges?

First, they used the price trick in the local market

Of the EUR 11bn of the industry sales in 2022, 57% are for the local German market. Until 2020, the local sales value of German confectionery has been decreasing since 2013. In 2020, a measure was taken to shift this trend.

The post-2020 increase in sales reflects more of a price increase than volume growth. The volume of confectionery products grew by 12%, while the value of those products rose by 25%. This indicates that the total revenue from confectionery sales has increased more than the quantity sold, potentially due to higher prices or a shift toward selling more premium products

It appears, that manufacturers may have transferred the burden of increased raw material costs and regulatory constraints to the end consumers.

Also, even if prices increased, this did not discourage us from buying more sweets and chocolates. This is what we can see in the chart below representing the evolution of the sales volume index and the sales value index. Let’s say in 2015, the price was 100 then in 2022 it price grew by 25%. If the demand was elastic, then a price increase would have decreased the volume and it would be represented in the chart by a volume inferior to 100.

In this case, the demand for confectionery is relatively inelastic, prices have increased by 25% and volumes have increased too by 12%. So, there is a willingness to pay more for confectionery items, which usually happens for products seen as necessities and/or with few substitutes on the market.

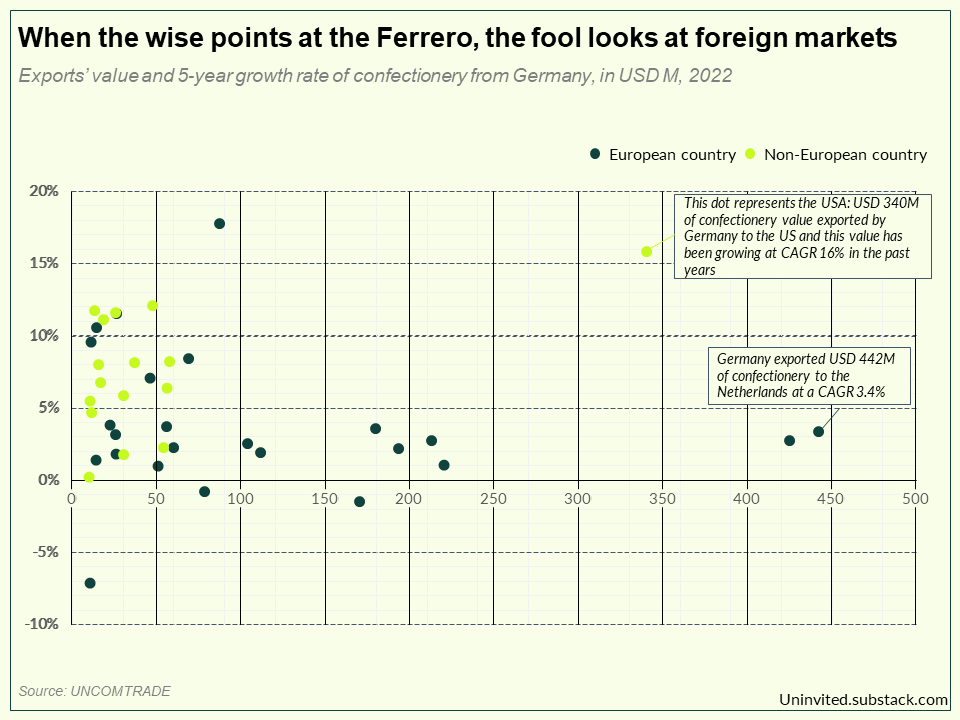

Then, they pursued opportunities in international markets.

In 2005, the German confectionery industry primarily catered to the domestic market, with 78% of sales occurring within Germany. By last year, domestic sales had decreased to 57%, with the industry expanding its reach abroad.

The local demand for German confectionery grew by CAGR 0.9% whereas the exports rose by 4.6% every year since 2010. So the importance of the local market has lowered as a response to the challenging context. Although European countries have been driving two thirds of the exports, the growth rate of German confectionery exports in the Eurozone is in general lower than in the emerging markets that have an untapped potential to be seized by these players.

The USA is an exception in this panorama as the third-largest destination and one of the highest-growing markets for German confectionery.

To navigate the challenging market, German confectionery companies capitalized on the price inelasticity of their products, strategically increasing prices domestically. Simultaneously, they expanded their focus on international markets, diversifying their revenue streams through exports, which now account for 43% of their total production value.

These two strategic levers might dry out at some point

Climate change will drive up commodity prices as it harms crop yields and quality. This was seen in the recent sugar shortages from leading producers like India, Brazil, and Thailand. Since raw materials are the main spend for confectionery manufacturers, they might pass these costs to the end consumers.

Another factor to take into account is obesity. With obesity affecting 19% of Germans and related health issues cutting life expectancy by 2.6 years, Germany—facing the highest overweight-associated health costs in the OECD—may soon tighten sugar regulations. As health costs soar, reaching EUR 30 billion, tax hikes on sugar seem inevitable, pushing confectionery prices up.

Climate change’s impact on raw materials costs and obesity’s impact on sugar regulation will add a strong premium to confectionery prices, that are today inelastic but to what extent? When comparing it to the tobacco industry (which also involves addiction, pleasure, and negative health impacts), cigarette taxes have indeed led to a reduction in sales.

In the short term, leveraging the price mechanism in the local market is unsustainable. The question is how long can the industry keep increasing prices before local consumers turn away from sweets, seeking alternative treats?

And at some point, the confectioners won’t find mercy either in foreign markets. Emerging countries, representing significant growth potential for manufacturers, will likely adopt EU-like stringent regulations for similar reasons. In the medium to long term, the window for export opportunities is expected to narrow

What would be the next sweet trick of German confectioners?

The limits of low-sugar-coating

If sugar is bad for health and confectioners are criticized for that, the natural idea is to reduce sugar right? But, cutting sugar from candy poses a dilemma. Sugar is central to candy's appeal, providing both flavor and a feel-good boost. Cut down the sugar, and you risk diminishing the very essence of what makes candy enjoyable. Removing it could mean losing that special something that keeps customers coming back. After all, we often turn to candy for that sugar rush.

This task is challenging, which is why we've seen only small, step-by-step innovations in creating low-sugar candies. Some leading companies like Haribo, whose products typically contain 47% to 68% sugar, are now offering low-sugar options with reduced sugar content ranging from 42% to 32%, this is still more than one-third of the gummies that are pure sugar.

To make sweets without sugar and still keep them delicious (and addictive), manufacturers need to focus and spend a lot on R&D.

Candy-balize

Cannibalization is a classic yet precarious innovation strategy and goes back to cautionary tales like Kodak's missteps and is contrasted by Apple's successful multiple self-disruptions.

What would be a cannibalization in the confectionery context? To find ideas, let’s look at niche markets in adjacent markets with high growth potential. For that, ladies and gentlemen, the matrix! I am positioning confectionery products in a two-line matrix: one for the effect on health and one for the impact on the body.

Confectionery products sit around the center of this matrix but the more the regulation increases on sugar the more down-left they will tend to be positioned. To escape that space, they could go to the upper right quadrant, this might mean branching into health-focused products that satisfy the sweet tooth while offering nutritional benefits. So basically following the shifting consumer values toward well-being without abandoning the core of what makes treats enjoyable.

In fact, the candies-as-supplements is a niche yet growing market and some companies are finding success there. They're making things like energy-boosting gummies or relaxing CBD chews that make “supplementation easy, enjoyable and effective”.

Beyond sweets

Confectioners are in the business of children’s interest and pleasure.

To find other revenue streams, they could go into other verticals of this market, beyond their core product including food and beverages, games, content/media, experience, and education.

This is what other players in the business of children’s pleasure did: Disney leveraged its animation roots to expand into Disneyland theme parks, then into physical and video games, and recently came back to media via the Disney Plus streaming platform. Lego also had a cross-vertical journey navigating from games to parks and discovery centers or even education apps.

Candy brands can use their strong association with children's enjoyment to enter new segments, if they trust you with their kids’ dental health why not with their entertainment?

If I was a decision-maker in the industry, what would be my next moves?

Acquire a Start-Up in the functional sweets segment, why?

It would set a foot in this niche yet growing markets

It would help the company build up quickly R&D capabilities

Most of these companies are digital native and Direct-to-consumers, I would use this opportunity to elevate my omnichannel strategy and gain customer intimacy

Start exploring the adjacent markets (media, games, experience,…)

Keep drying out the exports lever while it’s there

Thank you for reading. Two more things:

Since I'm new to the newsletter game, please reply to this email to share your thoughts and feedback

If you appreciated this post, please consider sharing it with someone or posting it on LinkedIn

Meryem

P.S.: As a thank you for reading through, here's a neat chart showing how confectionery sales change with the seasons. This chart focuses on B2B sales, which is why you'll see a big spike in October. This peak is due to the increased demand for sweets towards the end of the year.